Introduction

Blockchain technology is one of those terms people hear constantly, but often without a clear sense of what it actually changes.

It is usually mentioned in connection with cryptocurrency, yet the bigger story is not just about digital coins. It is about a different way to record information, verify activity, and build systems that do not depend entirely on a single central authority.

That is why blockchain technology has become such an important topic across finance, digital identity, recordkeeping, and other parts of the modern internet. It is no longer discussed only as an experiment behind Bitcoin. It is increasingly viewed as infrastructure that could support new kinds of digital systems and services.

In this guide, we’ll look at what blockchain technology is, how it works, why it matters, where it is being used, and what its strengths and limitations mean in practice.

Key Takeaways

- Blockchain technology is a decentralized system for recording and verifying information across a network of computers rather than relying on a single central authority.

- Data on a blockchain is stored in linked blocks, creating a chronological chain that helps protect the integrity of past records.

- Blockchain first gained widespread attention through Bitcoin, but its uses extend beyond cryptocurrency.

- Consensus mechanisms allow participants in the network to agree on which transactions or records are valid.

- Smart contracts allow certain blockchain systems to automate actions when predefined conditions are met.

- Blockchain technology is being explored in areas such as payments, supply chain tracking, digital identity, secure recordkeeping, and financial applications.

What Is Blockchain Technology?

Blockchain technology is a method of recording information in a shared digital ledger that is maintained across a network of computers rather than stored in a single central database.

In traditional systems, data is usually controlled by a central authority such as a bank, company, or government agency. That organization manages the database and determines who can add, modify, or access information.

A blockchain works differently. Instead of relying on a single central record, multiple participants maintain synchronized copies of the same ledger. When new information is added, the network verifies it according to agreed-upon rules before it becomes part of the permanent record.

Information on a blockchain is stored in groups called blocks. Each block contains a set of verified transactions along with a cryptographic reference to the block before it. These references connect the blocks together in chronological order, forming what is known as a blockchain.

Because each block is linked to the previous one, altering earlier data would require changing every subsequent block across the network. This structure makes the ledger extremely difficult to tamper with once information has been confirmed.

Blockchain technology first became widely known through Bitcoin, but the underlying system can be used to record many different types of information, not just financial transactions.

How Blockchain Works

To understand why blockchain technology is considered reliable for recordkeeping, it helps to look at the basic process through which information is added to the network.

Although different blockchain systems operate in slightly different ways, most follow a similar sequence of steps.

1. A Transaction Is Created

The process begins when a user initiates an action on the network. In cryptocurrency systems, this might involve sending digital assets from one wallet to another. In other blockchain applications, it could involve recording data such as ownership information, contracts, or other digital records.

For example, when someone sends Bitcoin to another user, the transaction request is broadcast to the blockchain network.

2. The Network Verifies the Transaction

Once the request is broadcast, computers in the network—often called nodes review the transaction to confirm that it follows the system’s rules.

These rules may include verifying that the sender has sufficient funds, confirming digital signatures, and ensuring the transaction format is valid.

To agree on which transactions are legitimate, blockchain networks rely on consensus mechanisms. Two widely used approaches include:

Proof of Work (PoW):

Used by Bitcoin, where specialized computers perform computational work to validate transactions and add new blocks.

Proof of Stake (PoS):

Used by networks such as Ethereum, where validators help secure the network by locking up cryptocurrency as collateral.

3. Transactions Are Grouped Into a Block

After validation, transactions are grouped together into a block.

Each block typically contains:

- a list of verified transactions

- a timestamp

- a cryptographic reference (called a hash) to the previous block

This reference connects each new block to the one before it.

4. The Block Is Added to the Chain

Once the block is approved by the network, it becomes part of the blockchain. Because each block references the previous one, altering any earlier data would require modifying every subsequent block across the network.

This makes tampering with past records extremely difficult.

5. The Network Updates

After a block is added, the updated blockchain is distributed across the network. Each participating node maintains a synchronized copy of the ledger.

This process allows blockchain networks to maintain a consistent and verifiable record of activity without relying on a single central authority.

Why Blockchain Matters

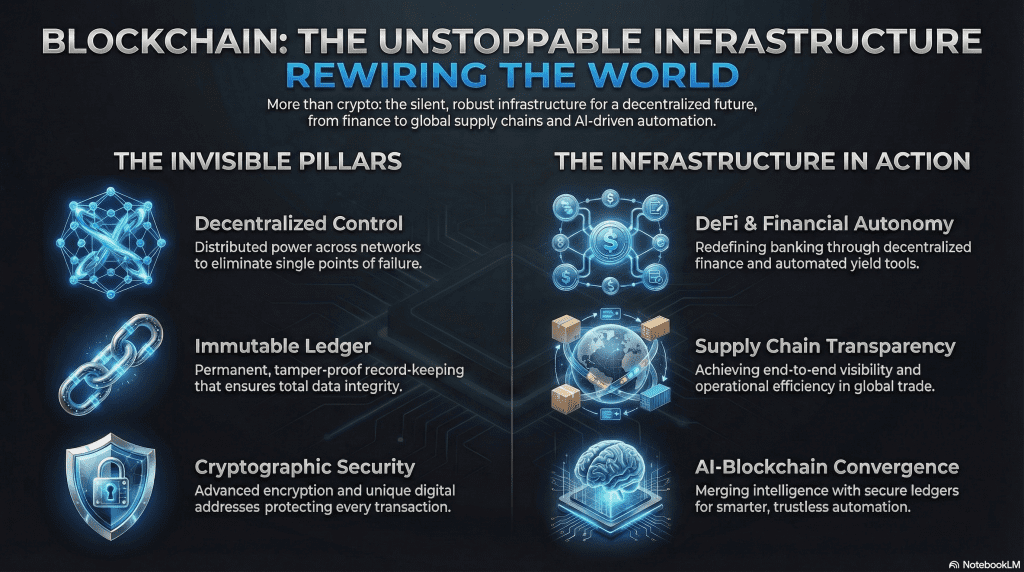

Blockchain technology introduces a different approach to managing information and transactions. Instead of relying on a single central authority to maintain records, blockchain networks distribute responsibility across many participants.

In traditional systems, trust is usually placed in intermediaries such as banks, payment processors, or database administrators. These organizations maintain records, verify transactions, and resolve disputes.

Blockchain systems approach this differently. By distributing the ledger across a network and using consensus mechanisms to validate updates, the system allows participants to agree on the state of the record without relying entirely on a central authority.

This structure creates several characteristics that distinguish blockchain from traditional databases.

Reduced Dependence on Central Authorities

Because blockchain records are maintained collectively by the network, transactions can occur directly between participants without requiring a central intermediary to process every interaction.

This model became widely known through systems such as Bitcoin, which allows users to send digital payments directly to one another without a traditional financial institution processing the transaction.

Shared Transparency

Many public blockchains allow participants to view transaction histories and verify how the network operates. This transparency allows users to independently audit activity rather than relying solely on reports from centralized organizations.

Data Integrity

Blockchain records are linked through cryptographic references between blocks. Once information has been confirmed and added to the chain, altering past records becomes extremely difficult without detection.

This structure helps protect the integrity of the ledger.

Network Resilience

Traditional databases often rely on centralized servers, which can create single points of failure. In contrast, blockchain networks distribute copies of the ledger across many nodes.

Because multiple participants maintain the system, the network can continue operating even if some nodes go offline.

Common Uses of Blockchain

While blockchain technology first gained attention through cryptocurrency, the underlying system can support many different types of applications. Because blockchain creates a shared, verifiable record across a distributed network, it is being explored in areas where transparency, security, and reliable recordkeeping are important.

Cryptocurrencies

The most widely known use of blockchain is cryptocurrency. Digital assets such as Bitcoin and Ethereum rely on blockchain networks to record transactions and verify ownership without requiring a central bank or payment processor.

Every transfer of cryptocurrency is recorded on the blockchain, allowing participants to verify balances and transaction histories through the network.

Payments and Cross-Border Transfers

Blockchain systems can also support payments directly between participants. In some cases, this approach can make international transfers faster or more accessible compared to traditional settlement systems.

Because blockchain networks operate continuously, transactions can be processed without the time limitations that sometimes exist in conventional banking systems.

Supply Chain Tracking

Businesses and organizations are exploring blockchain as a way to track goods as they move through supply chains. By recording product information at different stages of production, shipping, and delivery, blockchain can help create a transparent record of where goods originate and how they move through distribution networks.

Digital Identity and Recordkeeping

Blockchain technology is also being studied for digital identity systems and secure recordkeeping. In these cases, the goal is to allow individuals or organizations to verify credentials, ownership records, or other data without depending entirely on centralized databases.

Decentralized Finance (DeFi)

Another example of blockchain applications is Decentralized Finance (DeFi). DeFi refers to financial platforms built on blockchain networks that use smart contracts to automate services such as lending, borrowing, and trading.

Rather than functioning as a separate technology, DeFi demonstrates how blockchain infrastructure can support financial systems that operate through software rather than traditional intermediaries.

Benefits and Limitations of Blockchain Technology

Blockchain technology introduces a new way of managing data and transactions without relying on a single central authority. While this structure offers several advantages, it also presents technical and practical challenges that developers and organizations continue to address.

Benefits

Security Through Cryptography

Blockchain networks rely on cryptographic methods and distributed verification to secure data. Because information is recorded across many nodes rather than stored in a single centralized database, altering records without detection becomes extremely difficult once transactions are confirmed.

Transparency and Verifiability

Many public blockchains allow participants to view transaction histories and verify how the network operates. This transparency enables users to independently audit activity rather than relying solely on reports from centralized institutions.

Network Resilience

Traditional databases often depend on centralized servers, which can create single points of failure. Blockchain networks distribute copies of the ledger across many nodes, helping maintain system availability even if some parts of the network go offline.

Global Accessibility

Blockchain networks can be accessed from anywhere with an internet connection and compatible software. In financial applications, this can expand access to digital payment systems and other services for individuals who may not have access to traditional banking infrastructure.

Limitations and Challenges

Scalability

Many blockchain networks process a limited number of transactions per second compared with traditional payment systems. During periods of heavy activity, this can lead to slower processing times or higher transaction fees.

Developers are working on scaling solutions to improve performance, but many blockchain networks are still evolving in this area.

Smart Contract Vulnerabilities

Smart contracts enable automated systems on some blockchain platforms, but errors in the underlying code can create security vulnerabilities. If flaws exist in a contract, they may be exploited before they can be corrected.

Because blockchain transactions are typically irreversible, these vulnerabilities can sometimes lead to financial losses.

Regulatory Uncertainty

Legal frameworks surrounding blockchain-based services continue to evolve in many countries. Governments and regulators are still determining how existing financial and data protection laws apply to decentralized systems.

User Responsibility

Blockchain systems often give users direct control over their assets or accounts. While this independence can be beneficial, it also means individuals must manage private keys, verify transactions carefully, and protect themselves from scams or mistakes.

The Future of Blockchain Technology

Blockchain technology is still evolving, and many of the systems in use today represent early stages of what may become broader digital infrastructure. As development continues, several trends are shaping how blockchain networks are built and adopted.

Scaling Solutions

One of the main challenges for many blockchain networks is transaction capacity. To address this, developers are working on scaling solutions that allow more transactions to be processed efficiently.

One approach involves Layer 2 networks, which process transactions on secondary layers before recording the final results on the main blockchain. These solutions aim to increase transaction speed and reduce costs while maintaining the security of the underlying network.

Tokenization of Real-World Assets

Blockchain systems are increasingly being explored for the tokenization of real-world assets. This involves representing ownership of assets such as real estate, commodities, or financial instruments as digital tokens recorded on a blockchain.

Tokenization could simplify transfers of ownership, improve transparency, and potentially expand access to certain types of investments.

Cross-Network Interoperability

Many blockchain networks currently operate independently from one another. Developers are working on technologies that allow different blockchains to communicate and exchange data or assets more easily.

Improving interoperability could make it possible for multiple blockchain systems to function together within a broader digital ecosystem.

Institutional and Enterprise Adoption

Financial institutions, technology companies, and governments are increasingly researching blockchain applications. Some organizations are experimenting with blockchain-based settlement systems, digital identity solutions, and tokenized financial instruments.

In addition, several countries are exploring central bank digital currencies (CBDCs), which are digital forms of national currency inspired by blockchain-related technologies.

Ongoing Development

Blockchain systems continue to evolve as developers work to improve scalability, security, and usability. As these improvements progress, blockchain technology may become part of broader digital infrastructure used across financial services, data management, and global digital networks.

Final Thoughts: Blockchain as Digital Infrastructure

Blockchain technology is often discussed in connection with cryptocurrencies, but its broader significance lies in the infrastructure it provides for recording and verifying information.

By distributing records across a network and using consensus mechanisms to validate updates, blockchain systems offer an alternative way to manage data without relying on a single controlling authority. This approach can increase transparency, improve resilience, and allow participants to verify information through the network itself.

Because of these characteristics, blockchain is being explored for a wide range of applications, including financial systems, supply chain tracking, digital identity management, and secure recordkeeping.

Although the technology is still evolving, it represents a different model for building digital systems, one where verification can occur through shared networks rather than centralized control.

Understanding how blockchain technology works helps provide a clearer perspective on both the opportunities and the challenges associated with systems built on distributed ledgers.

Frequently Asked Questions

What is blockchain technology?

Blockchain technology is a distributed digital ledger that records transactions across a network of computers. Instead of relying on a central authority, the network collectively verifies and stores information, making records difficult to alter once they are confirmed.

Is blockchain only used for cryptocurrency?

No. While blockchain first gained attention through Bitcoin, the technology can support many other applications. Organizations are exploring blockchain for supply chain tracking, digital identity systems, secure recordkeeping, and financial infrastructure.

How do smart contracts work on a blockchain?

Smart contracts are programs stored on a blockchain that automatically execute actions when predefined conditions are met. For example, a smart contract might release funds after a transaction is confirmed or enforce the terms of a digital agreement without requiring a third-party intermediary.

Is blockchain technology secure?

Blockchain networks are designed to be highly secure through cryptographic verification and distributed data storage. Once transactions are confirmed and added to the chain, altering past records becomes extremely difficult. However, users must still protect their private keys and accounts to prevent unauthorized access.

Is blockchain regulated?

Blockchain technology itself is not directly regulated, but services built on blockchain networks may fall under legal and regulatory frameworks depending on the country. Cryptocurrency exchanges, digital asset platforms, and financial services using blockchain may be subject to regulation.

Can blockchain replace traditional financial systems?

Blockchain is unlikely to fully replace existing financial institutions in the near future. Instead, many experts expect blockchain technology to develop alongside traditional systems, with some organizations integrating blockchain infrastructure into their existing services.

Why is blockchain technology considered important?

Blockchain introduces a new way to record and verify information without relying entirely on a central authority. This approach can improve transparency, reduce reliance on intermediaries, and support new types of digital systems built on shared, verifiable data.

1 thought on “Blockchain Technology: How It Works and Why It Matters”