Introduction

Most investors start a Systematic Investment Plan (SIP) with a fixed monthly amount and keep that contribution unchanged for years. It is simple, predictable, and easy to maintain.

But income rarely stays the same over time. As careers progress, salaries often increase, and saving capacity often grows with them.

That raises a practical question for long-term investors.

If your income increases over the years, should your investments increase as well?

And if you gradually raise your monthly SIP contribution, how much difference would that actually make over the long run?

A step-up SIP calculator helps explore that scenario. By modeling how contributions increase over time, it allows you to compare different investment paths and see how compounding responds when the amount invested grows each year.

Before using the calculator, it helps to understand exactly how a step-up SIP works.

Disclaimer: Some links on this website are affiliate links. That means if you click and make a purchase, we may earn a small commission at no extra cost to you. The views expressed here are not official statements from any outside company.

What Is a Step-Up SIP?

A step-up SIP is a variation of a Systematic Investment Plan where the amount you invest increases periodically, usually once per year.

In a regular SIP, the monthly contribution stays the same throughout the investment period. With a step-up SIP, the contribution grows at a fixed percentage over time. This gradual increase allows the investment plan to adjust as your financial capacity improves.

For example, an investor might begin with a monthly investment of $200 and increase that amount by 10 percent each year.

The contributions would look like this:

Year 1: $200 per month

Year 2: $220 per month

Year 3: $242 per month

Year 4: $266 per month

Each increase may appear small on its own, but over many years the total invested amount becomes significantly larger than it would be with a fixed SIP.

The idea behind this approach is simple. As income grows over time, the investment contribution grows along with it. Instead of trying to make large jumps later, the increases happen gradually and become part of the long-term plan.

Understanding this structure makes it easier to see why some investors prefer step-up SIPs when planning for long investment horizons.

Why Some Investors Prefer Step-Up SIPs

A step-up SIP is designed to reflect how many financial situations evolve over time. Rather than keeping investments fixed for decades, the contribution gradually increases as earning capacity improves.

For some investors, this approach feels more natural than committing to a large monthly amount from the start.

One reason is income growth. Many professionals experience gradual salary increases throughout their careers. A step-up SIP allows investments to expand alongside that growth instead of remaining static.

Another consideration is inflation. Over long investment horizons, the purchasing power of money changes. Increasing contributions periodically can help investors maintain the real value of their savings efforts as costs rise over time.

There is also a behavioral advantage. Starting with a manageable investment amount can make it easier to begin and stay consistent. Instead of feeling pressured to invest a large amount immediately, investors can begin with a comfortable level and increase contributions gradually.

For these reasons, some long-term investors use step-up SIPs as a way to align their investment plan with how their financial life evolves.

How Much Difference Can a Step-Up Make?

At first glance, increasing a monthly investment by a small percentage each year may not seem like a major change. An extra 5 or 10 percent added annually can feel modest when viewed one year at a time.

Over longer periods, however, those incremental increases compound in two ways.

First, the total amount invested grows steadily because each year’s contribution is larger than the last. Instead of investing the same amount for decades, the investor gradually commits more capital over time.

Second, compounding begins to work on a larger base of contributions. As the investment amount increases, each future return is calculated on a growing pool of invested money.

The combination of these two factors can noticeably change long-term projections compared with a fixed SIP. Even moderate increases applied consistently over many years can lead to a very different total investment path.

This is exactly where a step-up SIP calculator becomes useful. Rather than estimating the impact manually, the calculator allows you to model different scenarios and see how annual increases affect the overall projection.

The next step is understanding how that calculator works and what information it uses to generate those projections.

What a Step-Up SIP Calculator Shows

A step-up SIP calculator is designed to estimate how an investment may grow when the monthly contribution increases periodically over time. Instead of assuming a fixed monthly investment, the calculator models a scenario where the contribution rises each year by a chosen percentage.

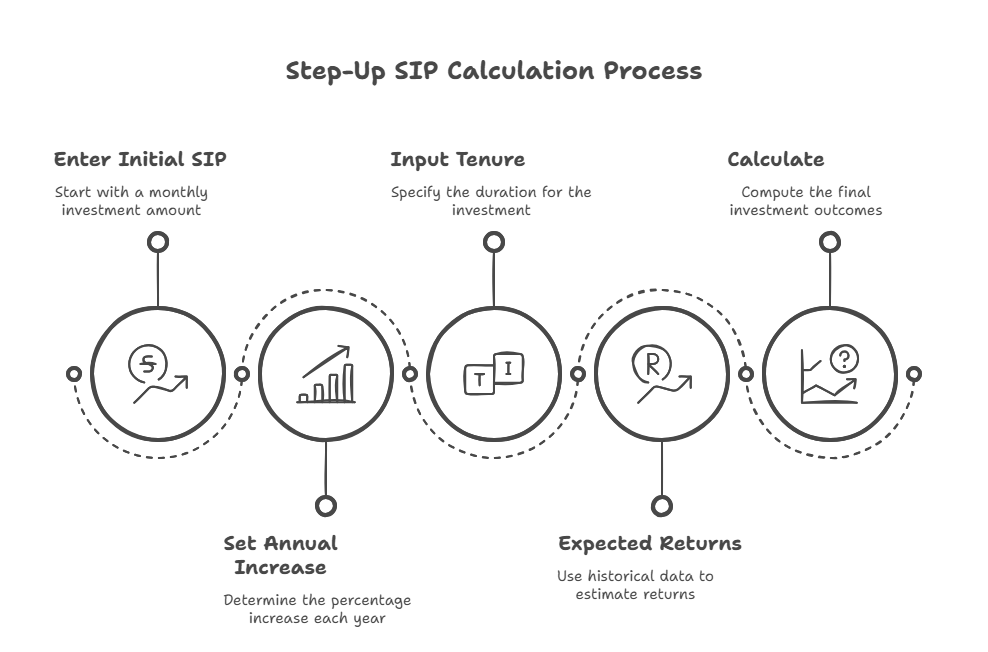

To generate this projection, the calculator typically asks for a few key inputs.

The first is the initial monthly investment. This represents the amount you plan to invest during the first year of the SIP.

The second input is the annual step-up rate. This is the percentage by which the monthly contribution increases each year. Many investors test scenarios such as 5 percent, 10 percent, or 15 percent increases.

Next is the investment duration. This determines how long the SIP will continue. Because SIPs are often used for long-term goals, many investors evaluate periods such as 10, 15, 20, or 25 years.

The final input is the expected annual return. This is an assumed average return used to estimate how the investment might grow through compounding over time.

Using these inputs, the calculator produces several outputs that help visualize the investment path.

It usually displays the total amount invested, the projected future value of the investment, and the estimated gains generated through compounding. Some calculators also provide charts or year-by-year breakdowns to illustrate how both contributions and returns evolve over time.

While these projections are based on assumptions rather than guaranteed outcomes, they provide a useful framework for comparing different contribution strategies and understanding the potential long-term impact of increasing investments.

How to Use a Step-Up SIP Calculator

Using a step-up SIP calculator is straightforward, but the value comes from exploring different scenarios rather than relying on a single estimate. A few small adjustments to the inputs can noticeably change the long-term projection.

Here is a simple process for working through the calculator.

1. Enter your starting monthly investment

Begin with the amount you are comfortable investing today. This will be the base contribution during the first year of the SIP.

2. Choose an annual step-up rate

Next, select the percentage by which the contribution will increase each year. Common values used for planning include 5 percent, 10 percent, or 15 percent. The key is to choose a rate that realistically reflects how your income may grow over time.

3. Set the investment duration

Specify how long you plan to continue the SIP. Long-term horizons such as 10, 20, or 30 years are often used when planning for major financial goals.

4. Enter an expected annual return

The calculator will ask for an assumed average return rate. This is not a guaranteed outcome but an estimate used to model how the investment might grow through compounding.

5. Review and compare the results

Once the inputs are entered, the calculator will display the projected value of the investment along with the total amount contributed over the chosen time period.

At this stage, it can be helpful to adjust the step-up rate or investment duration and compare different scenarios. This allows you to see how gradual increases in contributions may influence the overall investment path.

Step-Up SIP vs Regular SIP

Both regular SIPs and step-up SIPs follow the same core idea: investing a fixed amount at regular intervals over a long period of time. The difference lies in how the monthly contribution behaves as the investment plan progresses.

In a regular SIP, the investment amount stays the same throughout the entire duration. If an investor begins with $200 per month, that contribution remains $200 every month unless the investor manually changes it.

A step-up SIP, on the other hand, increases the contribution periodically, most often once per year. The increase is usually applied as a fixed percentage, allowing the monthly investment to grow gradually over time.

This distinction leads to different planning considerations.

Regular SIPs are often preferred by investors who value simplicity and stability. A fixed contribution makes budgeting predictable and removes the need to adjust the investment plan regularly.

Step-up SIPs are sometimes chosen by investors who expect their income to increase over time. By raising contributions gradually, the investment plan can evolve along with earning capacity rather than remaining static.

Another difference appears in the total amount invested over the long term. Because contributions increase periodically in a step-up SIP, the total invested amount typically becomes larger compared with a fixed SIP over the same time horizon.

Neither approach is universally better. A regular SIP may work well for investors who want a consistent commitment that fits comfortably within their budget. A step-up SIP may suit those who prefer a plan that scales gradually as their financial situation changes.

Understanding these differences helps investors choose a contribution strategy that aligns with their income patterns and long-term goals.

What If You Do Not Have a Step-Up SIP Calculator?

Not every investment tool includes a dedicated step-up SIP feature. If your calculator only supports fixed monthly contributions, you can still approximate the effect of increasing investments by breaking the plan into phases.

This approach requires a few additional steps, but it provides a reasonable estimate of how rising contributions might influence long-term projections.

1. Divide the investment period into segments

Start by splitting your total investment horizon into several blocks. For example, a 15 year plan could be divided into three five-year periods.

2. Set the contribution for the first segment

Enter your starting monthly investment for the first block of years and run the calculation using your chosen expected return.

3. Increase the contribution for the next segment

Apply your planned step-up rate to determine the new monthly investment for the following period. For example, if the original contribution was $200 and the increase rate is 10 percent per year, the contribution will be higher by the time the next phase begins.

4. Run the calculator again for each segment

Repeat the process for each block using the adjusted monthly contribution.

5. Combine the projected values

Add the results from each segment together to approximate the overall projection.

This method will not be as precise as a dedicated step-up SIP calculator because the increases are applied in larger blocks rather than every year. However, it can still provide a useful estimate when planning different contribution strategies.

Limitations to Be Aware Of

Step-up SIP calculators are helpful planning tools, but their results are based on assumptions rather than guaranteed outcomes. Understanding their limitations can help you interpret projections more carefully.

Assumed returns may not match real market performance

Most calculators ask for an expected annual return to estimate how the investment might grow. In practice, markets do not produce the same return every year. Some years may perform better than expected, while others may underperform. The projection reflects an average assumption rather than a precise forecast.

Taxes and investment costs may not be included

Many calculators focus on investment growth and may not factor in taxes, fund expenses, or platform fees. These costs can affect the final value of an investment over long periods, especially in larger portfolios.

Inflation affects future purchasing power

The projected value displayed by a calculator is usually shown in nominal terms. Over long time horizons, inflation can reduce the purchasing power of future money. Without adjusting for inflation, the projected value may appear larger than its real future value.

Consistency is assumed throughout the investment period

Calculators typically assume that contributions will continue on schedule and that the step-up increases will occur every year as planned. In reality, life events, income changes, or unexpected expenses may affect the ability to maintain those contributions.

Because of these factors, projections from a step-up SIP calculator should be viewed as planning estimates rather than precise predictions. They are most useful when comparing different strategies and understanding how contribution changes may influence long-term outcomes.

Planning Your Contribution Strategy

Deciding whether to increase SIP contributions each year is ultimately a budgeting decision. The strategy works best when the planned increases remain realistic and sustainable over time.

One practical approach is to begin with a monthly investment that fits comfortably within your current financial situation. Starting with a manageable contribution makes it easier to maintain consistency, which is one of the most important factors in long-term investing.

As income grows, contributions can be reviewed periodically and adjusted when appropriate. Some investors choose to increase their SIP after salary adjustments, bonuses, or other improvements in financial stability. These incremental changes allow the investment plan to evolve without placing sudden pressure on monthly cash flow.

It can also be useful to revisit the investment plan once a year. During that review, investors may choose to increase contributions, keep them unchanged, or adjust the strategy depending on their financial priorities.

A step-up SIP works best when increases happen gradually and remain aligned with actual income growth rather than aggressive projections. A steady and sustainable approach often supports better long-term consistency than a plan that becomes difficult to maintain.

Conclusion

A fixed monthly investment can be a practical starting point for long-term investing. It provides structure and helps build the habit of contributing regularly.

For investors whose income may increase over time, a step-up SIP offers another way to think about contributions. Instead of keeping the investment amount unchanged for many years, the contribution gradually grows as financial capacity improves.

Even modest increases applied consistently can change the overall investment path. A step-up SIP calculator makes it easier to explore these possibilities by showing how different contribution patterns may affect long-term projections.

While no calculator can predict future market performance, these tools can still provide valuable perspective when planning investment strategies. By testing different scenarios and reviewing assumptions carefully, investors can build a contribution plan that remains realistic, flexible, and aligned with their long-term goals.

Frequently Asked Questions

What is a step-up SIP calculator?

A step-up SIP calculator is a tool that estimates how an investment might grow when the monthly SIP contribution increases periodically, usually once per year. It combines the effect of increasing contributions with compound returns to project a possible future value.

How is a step-up SIP different from a regular SIP?

In a regular SIP, the monthly investment amount stays the same throughout the investment period. In a step-up SIP, the contribution increases at a fixed percentage over time, allowing the investment amount to grow gradually as income changes.

What step-up rate do investors typically choose?

The step-up rate varies depending on income growth and budgeting flexibility. Some investors use annual increases between 5 percent and 15 percent, but the appropriate rate depends on personal financial circumstances.

Can I simulate a step-up SIP using a regular SIP calculator?

Yes. If a calculator does not support step-up inputs directly, you can run multiple projections with different monthly contribution amounts to approximate how increasing investments might affect long-term projections.

Are projections from SIP calculators guaranteed?

No. SIP calculators use assumed return rates to estimate potential outcomes. Actual investment results depend on market performance, investment choices, taxes, and other factors.

1 thought on “Step-Up SIP Calculator: See What Annual Increases Can Do”

Comments are closed.